0x12…qrst

Welcome to the future of finance, where digital currencies are coming a reality! Central Bank Digital Currency (CBDC) is the new kid on the block(chain), and it is set to revolutionize the way we think about money.

But what can we expect from central banks worldwide as they navigate this brave new world? Let’s dive in!

The Rise of CBDCs

CBDCs are a new form of digital money issued by central banks for use by households and businesses. They’re not cryptocurrencies or digital assets but a digital version of a country’s national currency. This means CBDCs are regulated and backed by a central authority.

What Is the Role of CBDCs in the Global Landscape?

CBDCs are being explored by over 130 countries, representing 98% of the global economy. From the United States to Georgia, from Singapore to Switzerland, central banks are piloting or considering the launch of their own digital currencies.

We have to split CBDC into two categories:

· Wholesale CBDC that is aimed to be used by central and commercial banks for settlement payment

· Retail CBDC that caters for a retail audience (aka the regular folks) for daily use

In Singapore, the Monetary Authority is planning to conduct live trials for issuing wholesale CBDCs. Meanwhile, Georgia is collaborating with Ripple for their CBDC pilot. Even the Swiss National Bank is piloting a real Swiss franc wholesale CBDC with commercial banks.

It is interesting to note that most of the CBDC projects are related to wholesale and not retail (for now).

Pretty soon, we’ll be telling our grandkids, “Back in my day, we used to have something called ‘cash,’ and you could fold it into little origami animals. Kids these days just tap their digital wallets and call it a day.”

What Should We Expect from CBDCs?

CBDCs hold the promise of advancing global financial inclusion. Ripple’s Vice President for CBDC Engagements, James Wallis, underscores this transformative potential, highlighting how CBDCs can extend financial services to individuals worldwide, especially those with low income and no ties to financial institutions.

The managing director of the International Monetary Fund, Kristalina Georgieva, also urged the public sector to prepare to deploy CBDCs, stating that can replace cash and help financial inclusion.

Is It Too Soon or Can We Manage?

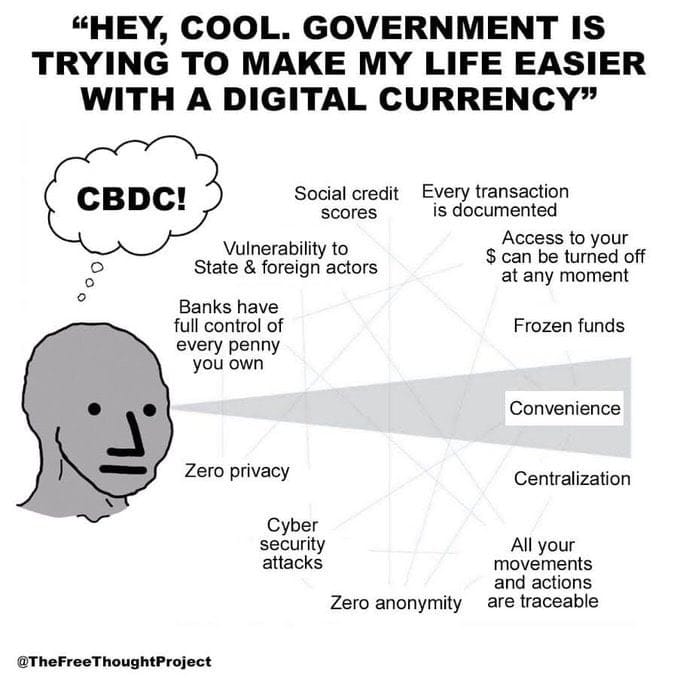

After blaming cryptocurrencies for everything, looks like the central banks now understand the potential of blockchain technology but want to keep the power of money for them by introducing CBDCs that will still be controlled by the same institutions that are managing fiat currencies today.

While the potential benefits are significant, there are also challenges to consider. For instance, a macroeconomics expert predicts a banking sector collapse in March 2024, linked to CBDCs. There could also be a significant pushback from people all over the world if cash will disappear. Most developing countries are still mostly running on cash, and privacy advocates have identified CBDCs as a global risk for freedom in the world.

The Future of CBDCs

As we look to the future, it’s clear that CBDC will play a crucial role in the evolution of the global financial system. So, as we stand on the brink of a new еra, one thing is certain: the world of finance as we know it is about to change.

All we can say is, with central banks worldwide gearing up to embrace such an enormous change, will privacy prevail or will it fall due to the rise of government control over everything?